Back in 2020, Tata launched the Nexon EV and had almost no competition worth mentioning. In those years, holding 70 to 80 per cent of India’s EV market was not a triumph of strategy. It was just the reality of being the only serious player in the room. The company deserves credit for taking the risk early, but that early advantage has now become a comfortable story that hides a more complicated picture.

The number Tata most often cites is its cumulative market share, which sits around 66 per cent when you add up all EV sales since the segment began. That figure sounds commanding. But it is basically a historical artefact. The years when Tata was selling three out of every four EVs are what inflate that cumulative number, not what is happening in showrooms today.

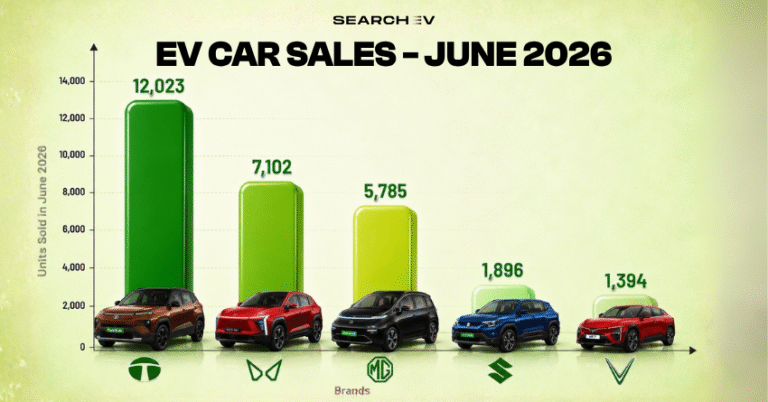

Tata Motor’s EV Share Drops Year After Year

In 2023, Tata held 73 per cent of annual EV sales. By calendar year 2024, that had fallen to 62 per cent. In 2025, it dropped again to 40 per cent. The company sold 70,194 units in 2025, which is actually a 13 per cent increase in volume over the year before. So Tata is selling more cars. But the market is growing so much faster that its share keeps shrinking.

India’s total EV passenger car market sold 177,630 units in 2025, a record. By January 2026 alone, the segment clocked 18,042 units in a single month, which is 51 per cent higher than the same month a year earlier. When the whole pie grows that fast, even a brand selling more cars can end up with a smaller slice.

Windsor Took the Crown

The single biggest story of India’s EV market in 2025 is the MG Windsor. It sold over 46,375 units last year and became the best-selling electric car in the country, taking the title from the Nexon EV that had held it for years. JSW MG Motor India’s total EV sales reached 51,603 units, which is a 136 per cent jump from the year before. For context, Tata grew 13 per cent in the same period.

What MG did differently was not just pricing. The Windsor introduced a battery-as-a-service model that lets buyers pay for the car without paying for the battery upfront, cutting the purchase price by roughly half. This removed the biggest mental block most Indians have about buying an electric car. Tata has not matched this approach, and industry analysts say that specific innovation is a large reason why MG’s market share jumped from 5 per cent in 2023 to 29 per cent in 2025.

Tata Motors’ EV vs MG: Where the Real Shift Is Happening

Right now, the real story in India’s EV market isn’t who started early, it’s who’s moving faster. Tata Motors still leads in total sales, but MG Motor India is catching up quickly.

In 2025, Tata sold more cars overall. But MG grew much faster, and that’s what’s changing the market. The big moment came when the MG Windsor EV overtook the Tata Nexon EV to become the best-selling EV. That wasn’t just about the car itself. MG made EVs feel more affordable by letting buyers skip the battery cost upfront, which directly tackled the biggest hesitation people have.

Tata hasn’t really matched that move yet. Its cars are still strong, but the approach is more traditional. And in a market that’s growing this fast, that difference matters.

Fleet Sales Collapsed Badly

One number that rarely gets mentioned in Tata’s positive coverage is what happened to its fleet sales. In 2023, the company moved 26,000 units to fleet operators. In 2024, that number fell to just 2,000. Two factors drove this. First, the FAME-II government subsidy scheme ended in March 2024, which had made fleet purchases financially attractive. Second, BluSmart, one of Tata’s biggest fleet customers with a committed order of 18,000 vehicles, collapsed entirely.

Tata’s own management admitted that almost the entire decline in EV sales could be attributed to lower fleet demand. This matters because it means retail buyer demand was never as strong as the headline sales numbers suggested. A chunk of Tata’s dominance was institutional buying driven by subsidies, not organic consumer preference.

Service Quality Hurting Growth

Tata’s own executives have acknowledged software quality problems and inadequate service infrastructure in key cities. The company publicly identified 21 hotspot cities where customer experience was below acceptable levels. For a brand asking people to make a significant financial commitment to a new technology, this kind of friction is expensive in ways that do not show up immediately in sales data but absolutely show up in word of mouth.

What makes this more pointed is that Tata launched major new products during this period, including the Curvv EV and updated Nexon EV variants. New launches usually move the needle. They did not reverse the share decline. That tells you the issue is not product quality alone. It is perception, service experience, and the arrival of credible alternatives at similar price points.

Mahindra Is Watching Closely

Beyond MG, Mahindra is quietly becoming the third threat. Its born-electric platform produced the BE 6e and XEV 9e, and the brand’s EV share of its own sales has been rising steadily. It held roughly 14 per cent of the EV market in 2025 and by February 2026 was nudging toward 22 per cent on some monthly counts. Maruti has also entered the space with the e-Vitara. Hyundai’s Creta Electric has already proven popular.

Tata is no longer fighting one challenger. It is managing a multi-front erosion while trying to keep up with product launches, fix its service network, and rebuild retail confidence simultaneously.

What Tata Has Going for It

None of this means that Tata is going down. It still sold more EVs than anyone else in India in 2025. Its charging infrastructure plans are genuinely ambitious: 400,000 charge points, including 30,000 public fast chargers by 2027. If it delivers on that, it creates real lock-in for owners and a tangible reason for new buyers to pick the brand.

The Sierra EV, a new Punch EV, and the Avinya range are all coming in 2026. The product pipeline is active. Tata’s own CCO said internally that the 70 per cent-plus share was never sustainable, and a more realistic target is staying above 50 per cent. Early 2026 trends suggest the share remains in the mid-40 per cent range, so it is right on that line.

The Real Picture

India’s EV market is at just 4 per cent penetration of total passenger vehicle sales. That means 96 per cent of buyers have not yet bought an EV. The opportunity is enormous, but it also means no brand has deep loyalty to protect. Every new buyer is up for grabs.

Tata is still the leader, but the idea of dominance no longer holds the same weight. What looks like control on paper is increasingly a story of early advantage, while the current market is far more competitive and evenly contested. That gap between historical dominance and current reality is where the perception starts to break.